Investing 101: Understanding Financial Reporting

| Date of Inversion | Recession Start (Days) | S&P 500 Top (Days) | S&P 500 Bottom (Days) | Housing Market Top (Days) | |

|---|---|---|---|---|---|

| October 25, 2022 | N/A (too recent) | N/A (too recent) | N/A (too recent) | N/A (too recent) | |

| August 19, 2019 | 182 (December 1, 2019) | 14 (September 2, 2019) | 422 (March 23, 2020) | Difficult to pinpoint (Estimated Range: N/A) | |

| August 24, 2006 | 18 (December 16, 2006) | 210 (June 5, 2007) | 518 (July 2, 2009) | 396 (Estimated Range: Early 2011 to Mid-2012) | |

| February 2, 2000 | 273 (December 1, 2000) | 189 (July 18, 2000) | 1365 (October 9, 2002) | Difficult to pinpoint (Estimated Range: Mid-2001 to Mid-2002) | |

| June 30, 1989 | 120 (October 30, 1989) | 63 (September 13, 1989) | 540 (May 18, 1990) | 210 (March 1989 peak) | |

| March 29, 1973 | 150 (July 18, 1973) | 90 (June 11, 1973) | 486 (February 4, 1975) | 30 (April 1973 peak) | |

| December 13, 1965 | 90 (March 14, 1966) | 60 (February 11, 1966) | 630 (August 1969) | 90 (February 1966 peak) | |

| September 1, 1957 | 180 (March 1, 1958) | 120 (December 31, 1957) | 720 (September 1960) | 150 (February 1957 peak) | |

| May 9, 1956 | 210 (December 1, 1956) | 60 (July 17, 1956) | 810 (January 22, 1958) | 270 (August 1956 peak) | |

| July 14, 1953 | 9 (December 23, 1953) | (No recession) | 330 (April 26, 1954) | 90 (October 1953 peak) | |

| Average | 132.2 | 94.8 | 636.4 | 189.8 |

"Annuity" refers to an insurance contract issued and distributed by financial institutions with the intention of paying out invested funds in a fixed income stream in the future for a certain number of years or a lifetime.

Tax Implications:

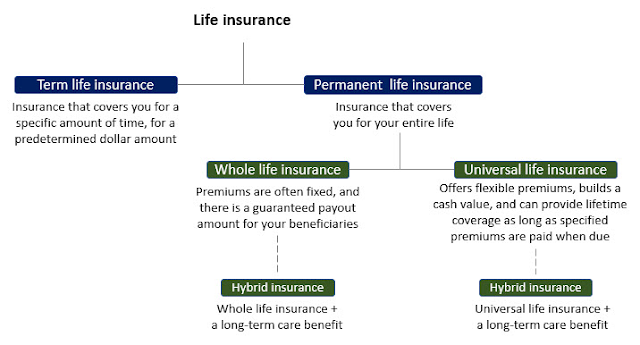

Life insurance generally falls into 2 categories: Term and permanent:

| Feature | Term | Whole | Universal | Variable |

|---|---|---|---|---|

| Death benefit | Guaranteed as 1-time lumpsum | Guaranteed in a lump sum or in installments. | Guaranteed in a lump sum or in installments. | Guaranteed in a lump sum or in installments. |

| Premiums | Low | High & Fixed | Variable. You must pay at least enough to cover the cost of insurance and the administration charges. | Variable |

| Cash value | None | Guaranteed | Guaranteed or variable | Variable |

| Investment options | None | None | Limited | Varied |

| Surrender charges | No | Yes or no | Yes or no | Yes |

| Tax treatment | Tax-deferred | Tax-deferred | Tax-deferred | Tax-deferred |

| Pros | Affordable, short-term coverage to give your loved ones a lump sum to help replace the loss of your income | Guaranteed death benefit, guaranteed cash value, low fees. eligible to earn dividends based on the company's earnings. | Flexibility, death benefit can be increased, cash value can be used for loans or withdrawals | Investment options, potential for higher returns |

| Cons | Temporary coverage, death benefit can decrease if premiums are not paid | High premiums, low investment returns. | Higher premiums than whole life, death benefit can decrease if cash value is withdrawn | Potential for losses, higher fees than whole life |

Disclaimer:

It is important to note that the dates below are just general guidelines. The specific dates for a particular dividend may vary depending on the company's policies. Investors should always check with the company directly to confirm the dates for any dividend that they are interested in receiving.

| Date | Name | Significance |

|---|---|---|

| Declaration date | The date on which the company's board of directors announces the dividend. | This is the first date that investors can know for sure whether or not a dividend will be paid. |

| Ex-dividend date | The date one day before the record date. | On this date, the stock price typically drops by the amount of the dividend. New buyers of the stock after this date will not be entitled to receive the dividend. |

| Record date | The date on which the company determines who is entitled to receive the dividend. | Investors must be listed as shareholders on the company's books as of this date in order to receive the dividend. |

| Payable date | The date on which the company actually pays the dividend to shareholders. | This is the date that shareholders will actually receive the dividend in their accounts. |

Following are all the points to remember for the 529 Post Tax Education investment account:

STEPS:

BASIC STEPS:

Following are all the ways in which you can reduce your yearly taxable income:

PROTIP Section 0: Use your standard deductions

This depends on your marital status and number of dependents.

File your taxes ASAP as that starts your Audit timeline early

If your tax return does have errors, the timeframe in which the government has to prove your fault starts decreasing earlier.

PROTIP Section 1: Maximize Pre-Tax & Post-tax Contributions

PROTIP Section 2: Maximize your Non-taxable income

(no need to add these to your tax return)

PROTIP Section 3: Get Married

(If you're legally married as of December 31 of the tax year, the IRS considers you to be married for the full year.)

C) Use Spouse's income to increase Total IRA contributions:

Couples filing jointly can make contributions to two separate IRA accounts – one for each spouse where the unemployed spouse (taxpayer with SSN), can contribute to an IRA using their spouse's income.

D) Increase primary residence sale tax-free profit limit from $250,000 to $500,000:

To qualify for the larger $500,000 tax-free gain, both spouses must have lived in the home for at least two of the last five years, and at least one spouse must have owned the home for at least two of the last five years.

1) If filing jointly: